How your contributions work

During your working lifetime, your employer will pay into a superannuation account for you at the current rate of 9.5% of your salary. These payments will continue until you retire.

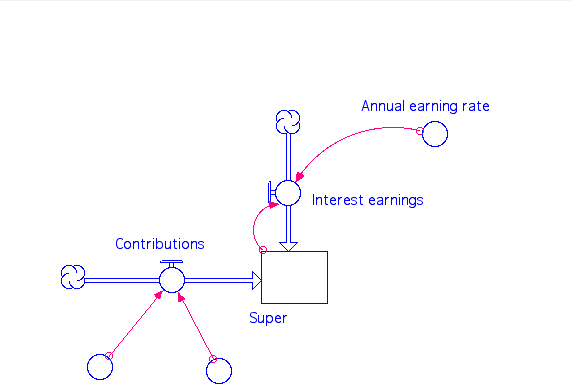

A simple System Dynamics model of your super account during your working life looks like this.

This model is based on your earning $60,000 year throughout your working life from age 20 to retirement at 65. While this is a simplification of what really happens, it helps to keep things simple in the early stages of an explanation of superannuation.

In this model

Contributions = Salary * Contribution rate

Interest Earnings = (Accumulated) Super * Annual earning rate

The earnings from the stock market are constant at a conservative 5% in the model. Recently stock market returns have been much higher than this. I will discuss the impact of this later in the article.

There are two revenue flows into your superannuation account. The first is your contributions: 9.5% of your salary.

The second revenue flow is the interest earnings on your accumulated superannuation. This will be the earnings rate if the funds are invested in the stock market, as is the case with most superannuation funds.

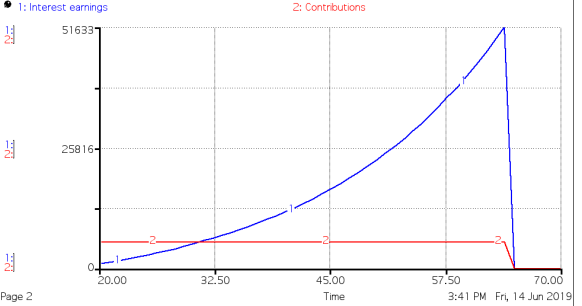

The contribution that these two flows make is quite different.

While your contributions have remained stable at $5700 pa, however the interest earnings have risen to just below $52,000 in your final work year. This is because the interest on your account compounds giving the account exponential growth.

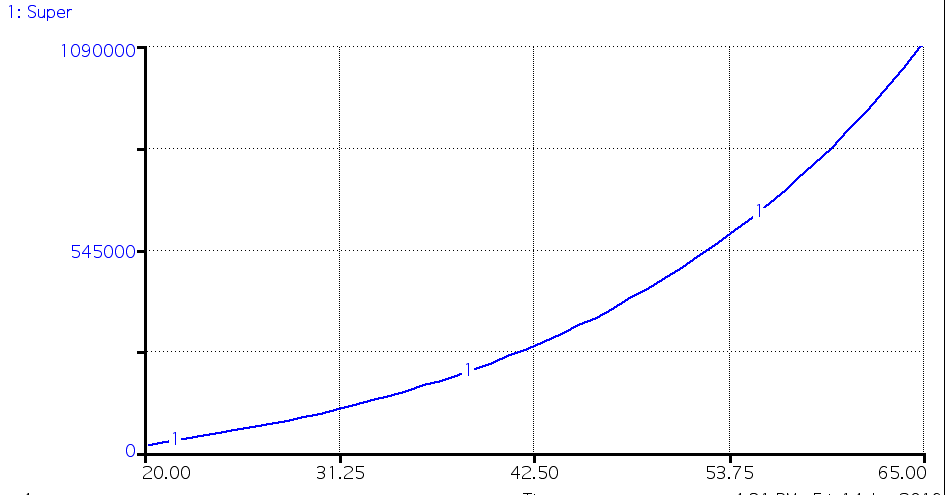

As a consequence of this growth, your accumulated super fund now holds just under $1.1 million

Withdrawing money for a home deposit

There is periodic discussion about allowing first-time buyers to draw on their superannuation for a deposit on their house.

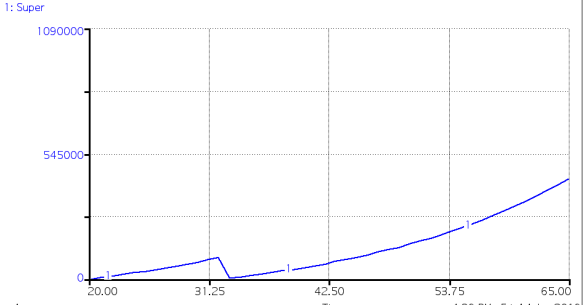

This iteration of the model shows the impact of withdrawing $100,000 for a home deposit at the age of 32.

As a result, the accumulated superannuation at 65 has now dropped to $434,000, just over 1/4 of the final retirement total, had the withdraw not been.

Such a decline will have a profound impact on your final retirement superannuation payments.

The reason for this dramatic difference is that you go into the final high earning 10 years of your superannuation fund on a much lower base and, as a consequence, the earnings from interest are much lower.

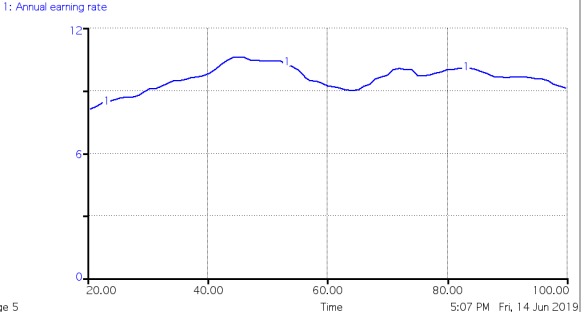

What happens if the earnings rate from the stock market varies

This will make a huge difference to your accumulated superannuation when you retire.

If the simulation varies the returns over the period of investment, particularly in this case varying the rate above 5%, the outcome is quite marked.

Here is rate at which the market returned varies.

This represents an annual return of 9%, well within the range of the ASX 500 has been performing at over the last 20 years.

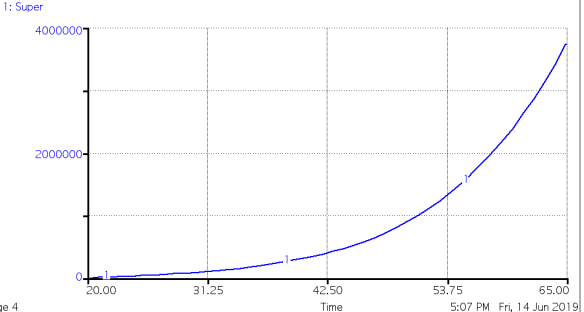

The impact of this variation, well above the 5% in the first simulation, is shown in the next graph.

The accumulated Super is now $3.4 million.

The size of accumulated superannuation funds, such as the one modelled here, raises some important questions about the nature and function of superannuation which will be discussed in a later article.

I read a good deal of posts here. Probably you spend a lot of time writing, Thanks

for sharing!

King regards,

Thompson Dencker